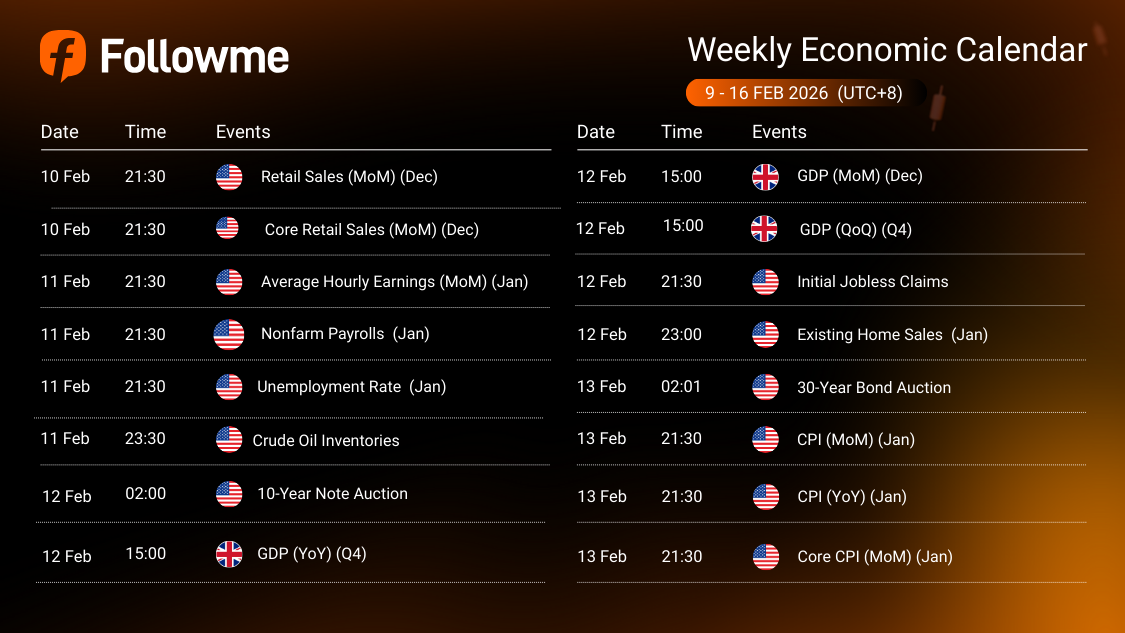

Weekly Economic Calendar: Week of February 9 - 16, 2026 (GMT+8)

This week’s macro calendar is dominated by U.S. labor + inflation data, with U.S. Nonfarm Payrolls + Unemployment Rate + Average Hourly Earnings (Wed 21:30) and U.S. CPI (MoM/YoY) + Core CPI (Fri 21:30) acting as the main USD volatility anchors (UTC+8). Early in the week, U.S. Retail Sales + Core Retail Sales (Tue 21:30) set the tone for consumption strength and can quickly reprice yields and risk sentiment. Mid-week, Crude Oil Inventories (Wed 23:30) may trigger energy-linked swings, while Japan’s National Founding Day (Wed, Holiday) could slightly thin Asia-session liquidity. Outside the U.S., UK GDP (YoY/MoM/QoQ) (Thu 15:00) is the key GBP risk event, followed by U.S. Initial Jobless Claims (Thu 21:30) and Existing Home Sales (Thu 23:00) as important “confirmation checks” for growth and rates expectations. Finally, keep an eye on U.S. duration supply via the 10-Year Note Auction (Thu 02:00) and 30-Year Bond Auction (Fri 02:01), which can amplify moves in yields heading into the CPI-driven close-of-week positioning.

| Time | Cur. | Events | Fcst | Prev |

| USD | ||||

| USD | ||||

| Average Hourly Earnings (MoM) (Jan) | ||||

| Nonfarm Payrolls (Jan) | ||||

| Unemployment Rate (Jan) | ||||

| Crude Oil Inventories | ||||

| GDP (MoM) (Dec) | ||||

| GDP (QoQ) (Q4) | ||||

| Initial Jobless Claims | ||||

| Existing Home Sales (Jan) | ||||

| 30-Year Bond Auction | ||||

| CPI (MoM) (Jan) | ||||

| CPI (YoY) (Jan) | ||||

| Core CPI (MoM) (Jan) |

| Key highlights: |

🇺🇸 Retail Sales (MoM) (Dec) – Tuesday 21:30

🇺🇸 Core Retail Sales (MoM) (Dec) – Tuesday 21:30

🇺🇸 Average Hourly Earnings (MoM) (Jan) – Wednesday 21:30

🇺🇸 Nonfarm Payrolls (Jan) – Wednesday 21:30

🇺🇸 Unemployment Rate (Jan) – Wednesday 21:30

🇺🇸 Crude Oil Inventories – Wednesday 23:30

🇺🇸 10-Year Note Auction – Thursday 02:00

🇬🇧 GDP (YoY) (Q4) – Thursday 15:00

🇬🇧 GDP (MoM) (Dec) – Thursday 15:00

🇬🇧 GDP (QoQ) (Q4) – Thursday 15:00

🇺🇸 Initial Jobless Claims – Thursday 21:30

🇺🇸 Existing Home Sales (Jan) – Thursday 23:00

🇺🇸 30-Year Bond Auction – Friday 02:01

🇺🇸 CPI (MoM) (Jan) – Friday 21:30

🇺🇸 CPI (YoY) (Jan) – Friday 21:30

🇺🇸 Core CPI (MoM) (Jan) – Friday 21:30

Macro Analysis:

🇺🇸 U.S. Growth Pulse (Retail Sales + Core Retail Sales) – Tue:

Consumer spending is the first big “growth check” of the week. A stronger print supports the resilience narrative (yields/ USD supported), while a weaker result can shift pricing toward slower growth and push risk sentiment more cautiously into the mid-week labor data.

🇺🇸 U.S. Labour Anchor (NFP + Unemployment + AHE) – Wed:

This is the main USD volatility anchor before CPI. Payrolls sets the headline tone, unemployment frames slack/tightness, and Average Hourly Earnings feeds directly into inflation sensitivity. A “hot” labor bundle typically lifts yields and supports USD; a softer bundle can trigger fast repricing lower in yields and a lighter USD tone.

🇺🇸 U.S. Labour Stress Check (Initial Claims) – Thu:

Claims acts as the near-term confirmation signal after NFP. Lower-than-expected claims reinforces tight-labor conditions (USD/yields supportive). Higher claims can validate cooling momentum and amplify any post-NFP risk-off / lower-yield move.

🇺🇸 U.S. Inflation Anchor (CPI + Core CPI) – Fri:

This is the week’s decisive repricing event. CPI (headline) shapes broad inflation expectations, while Core CPI typically carries the heavier policy/real-yield impact. Expect positioning to compress into the release, then expand quickly on surprise magnitude vs expectations.

🇺🇸 Rates Volatility Amplifiers (10Y Auction Thu + 30Y Auction Fri):

Treasury auctions can swing yields and curve shape, especially when they bracket the week’s biggest data. Weak demand can push yields up (supporting USD), while strong demand can ease yields and soften USD—often amplifying whatever narrative NFP/CPI sets.

🇺🇸 Energy → Inflation Sensitivity (Crude Oil Inventories) – Wed:

Oil moves can feed into inflation expectations and risk tone. A draw that lifts crude can keep inflation concerns “alive” into CPI; a build that pressures crude can cool inflation fears and support a softer rates impulse.

🇬🇧 UK GDP (YoY/MoM/QoQ) – Thu:

This is the key GBP risk event. Surprises can move GBP sharply and spill into broader USD flows through relative-rate repricing and risk sentiment, especially with U.S. claims/housing later the same day.

Speculative Outlook for USD Traders:

This is a labour-first, CPI-finish week. Expect fast repricing around Wed 21:30 and Fri 21:30, with auctions and oil acting as volatility multipliers.

Check out full here: Followme Economic Calendar Tool

Follow Followme for the newest market updates

면책 조항: 본 게시글에 표현된 견해는 전적으로 작성자의 견해이며 Followme의 공식 입장을 대변하지 않습니다. Followme는 제공된 정보의 정확성, 완전성 또는 신뢰성에 대해 책임을 지지 않으며, 서면으로 명시적으로 언급되지 않는 한 해당 내용을 기반으로 취해진 어떠한 조치에 대해서도 책임을 지지 않습니다.

- 끝 -